TEL:+86 158 1857 3751

TEL:+86 158 1857 3751

I. The Communication Cornerstone of the Smart Manufacturing Era

As global manufacturing accelerates its digital and intelligent transformation, industrial transceivers are playing an increasingly critical role. As core components of industrial communication systems, industrial transceivers convert electrical signals to optical signals and vice versa between various devices and networks, thereby enabling real-time monitoring, predictive maintenance, remote control, and other key applications. With the deep advancement of Industry 4.0 and the Industrial Internet of Things (IIoT), the industrial transceiver market is entering a period of rapid growth.

II. Market Size and Growth Trends

The global industrial transceiver market size is reflected in multiple statistical perspectives, highlighting the market’s breadth and complexity. According to reports from several market research institutions:

Future Market Report data shows that the global industrial transceiver market was approximately US$1.85 billion in 2024 and is projected to reach US$3.15 billion by 2032, with a compound annual growth rate (CAGR) of approximately 6.9% during the forecast period.

6Wresearch statistics indicate that the global industrial transceiver market was valued at US$1.4 billion in 2024 and is expected to reach US$2.02 billion by 2031, at a CAGR of 5.60%.

Reanin report provides a more optimistic estimate for the industrial network transceiver market: the market value is approximately US$9.817 billion in 2025 and is expected to surge to US$26.756 billion by 2032, representing a CAGR of 15.4%.

Focusing on the industrial optical transceiver segment, 360iResearch estimates the market size at approximately US$11.93 billion in 2025, growing at a CAGR of 9.58% to reach US$22.65 billion by 2032.

The above data discrepancies mainly stem from differing definitions of “industrial transceiver” across institutions – some focus on industrial Ethernet PHY transceivers, while others cover a broader range of industrial network communication devices.

From a regional perspective, North America holds approximately 32% of the market share, making it the fastest-growing region, while the United States alone accounts for about 18.9% of the global market, the largest single-country market. The Asia-Pacific (APAC) region contributes approximately 49% of the global industrial communication market, driven primarily by the leadership of countries such as China and Japan in 5G deployment and smart manufacturing.

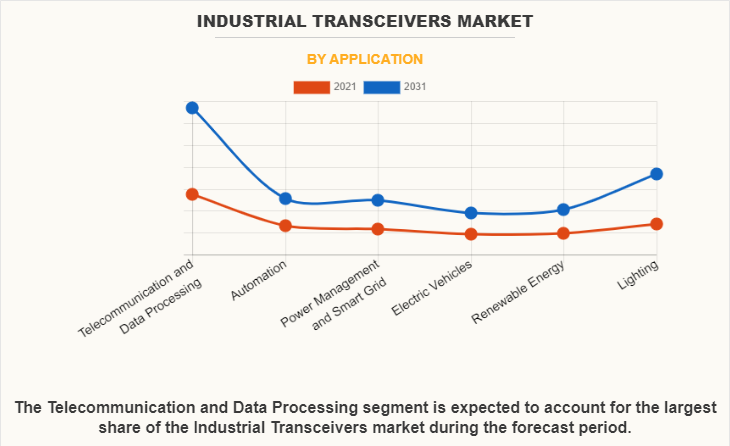

From a product structure perspective, wireless transceivers dominate with a 68% share, reflecting a significant trend toward wireless and flexible communication methods in the industrial sector. In terms of protocols, Ethernet, Fibre Channel, and SONET/SDH are the mainstream communication protocol types, supporting data exchange requirements across different industrial scenarios. From an application perspective, industrial automation, oil & gas, energy utilities, transportation, and building automation constitute the major end-user markets.

III. Key Market Drivers

1. Widespread Deployment of Industry 4.0 and Smart Manufacturing

The core of Industry 4.0 and smart manufacturing lies in real-time data collection, transmission, and analysis. As the underlying infrastructure enabling this goal, industrial transceivers directly benefit from global investment booms in smart factories. According to statistics, about 40% of industries are deploying advanced transceivers to achieve real-time data exchange and optimize production efficiency. The deep integration of Operational Technology (OT) and Information Technology (IT) further drives demand for highly reliable, long-distance, low-latency communication devices.

2. Rapid Growth of the Industrial Internet of Things (IIoT)

With the proliferation of IIoT applications such as sensor networks, asset tracking, and remote monitoring, industrial transceivers have become the critical bridge connecting the physical and digital worlds. The integration of low-power wide-area network technologies such as Zigbee, LoRaWAN, and NB-IoT enables transceiver designs to better meet the needs of sensor networks and asset tracking.

3. Digital Transformation of Critical Infrastructure

Sectors such as energy, power, and transportation are accelerating their digital upgrades. In scenarios such as smart grids, railway transportation, and oil pipeline monitoring, industrial transceivers must withstand harsh environments including extreme temperatures, vibration, and electromagnetic interference, driving demand for high-performance, durable transceiver products. Industrial Ethernet switches have been widely deployed in automotive manufacturing, oil exploration, offshore wind power, intelligent transportation, power energy, and many other fields, demonstrating the core value of transceivers in these scenarios.

IV. Key Technologies and Product Trends

1. Wireless and Low-Power Trends

Industrial communication is shifting from traditional wired solutions to wireless approaches. Low-power, long-range transmission technologies (e.g., LoRa, NB-IoT) are increasingly integrated into transceiver designs to meet application requirements for sensor networks and asset tracking. The rise of 5G private industrial networks is also opening new application spaces for industrial wireless communications.

2. High Speed and High Bandwidth Demands

As AI training, big data analytics, machine vision, and other applications enter industrial scenarios, industrial networks face ever-increasing demands for data transmission rates. Current transceiver products already cover data rates from 1Gbps to 400Gbps, and are moving toward 800Gbps and even 1.6Tbps. Industrial-grade optical transceiver data rates have evolved from 10G and 25G to higher speeds. Ethernet optical transceivers for AI cluster applications have become one of the main drivers of market growth.

3. Modular and Small-Form-Factor Designs

Pluggable form factors such as SFP, SFP+, QSFP, QSFP28, and CFP have become mainstream designs for industrial transceivers, enabling end users to flexibly configure networks for specific applications while facilitating maintenance and upgrades.

4. Edge Computing and Intelligent Integration

Next-generation industrial transceivers are integrating edge computing capabilities, allowing preliminary processing and decision-making close to the data source, thereby reducing latency and dependence on cloud infrastructure. The integration of AI and machine learning into industrial systems further drives demand for smarter transceivers to support automated decision-making and predictive maintenance.

5. Enhanced Security

As industrial communication systems face increasing cyber threats, secure data transmission and encryption capabilities have become standard features of new transceivers. Rising cybersecurity requirements are significantly influencing product innovation directions.

V. Competitive Landscape and Key Players

The global industrial transceiver market features a moderately fragmented yet highly dynamic competitive landscape. International giants and regional specialized manufacturers together form a diversified competitive ecosystem.

Global Industrial Automation Leaders: Siemens, ABB, Schneider Electric, and Rockwell Automation possess comprehensive product lines and deep technical expertise in industrial communications, giving them significant advantages at the system integration level.

Specialized Industrial Communication Equipment Providers: Moxa (Taiwan, China) and Advantech hold important positions in industrial Ethernet switches, serial device servers, and industrial wireless equipment. Additionally, brands such as Belden, Phoenix Contact, and Hirschmann enjoy high market recognition.

Optical Transceiver and Chip Suppliers: In the industrial optical transceiver field, major participants include Finisar, AMS Technologies, Analog Devices, Cisco Systems, Renesas Electronics, Infineon Technologies, and Texas Instruments. In the industrial-grade optical transceiver segment, Cisco, Juniper, ProLabs, Molex, and Broadcom also hold significant shares.

Market mergers, acquisitions, and strategic partnerships are frequent, with approximately 38% of industrial leaders using such strategies to enhance product interoperability and expand solution portfolios in response to rising demand from digital production frameworks.

VI. Future Outlook

Looking ahead, the industrial transceiver market will continue to evolve toward higher speed, lower power consumption, greater intelligence, and better security.

On the technology front, silicon photonics is expected to become a core innovation direction in the next phase. This technology integrates photonic and electronic devices on a single silicon chip, significantly improving data transmission efficiency and reducing energy consumption, aligning with the growing emphasis on sustainability in data centers and industrial networks.

On the application front, scenarios such as smart factories, smart grids, and autonomous transportation systems will open vast new markets for industrial transceivers. According to forecasts, the global industrial wireless transmitter market will grow from US$3.81 billion in 2025 to US$6.26 billion by 2031, at a CAGR of 8.63%. The industrial CAN transceiver market will also grow from US$212 million to US$343 million over the same period, at a CAGR of approximately 7.5%.

At the same time, the market faces certain challenges. Intensified competition, accelerated technology iteration, raw material price fluctuations, supply chain disruptions, and varying compliance certification requirements across regions are all issues that companies must actively address.

VII. Conclusion

The industrial transceiver market stands at the intersection of a new wave of technological change and industrial upgrading. As the critical link connecting the physical industrial world with the digital realm, its importance is increasingly evident in the era of Industry 4.0 and IIoT. From rapid market growth to continuous innovation in technology pathways, and from a diverse competitive landscape to expansive development prospects, this market demonstrates strong vitality and broad potential. For enterprises across the industry chain, grasping the four major trends – wireless, high-speed, intelligent, and secure – and deeply cultivating specific application scenarios will be key to winning future competition.

>

>

>

>

>

>

>

>

>

>

>

>